Using a Charitable Gift Annuity in a Client’s Financial Plan

For several hundred years, charitable gift annuities have been a common planned gift solution in the United States. The first such gift was established in 1830 between John Trumbull and Yale College. Yale was to pay Trumbull “a competent annuity for the remainder of my life” in exchange for over 100 of his paintings. Trumbull was a widely known artist and is most remembered for the numerous murals in the U.S. Capitol rotunda.

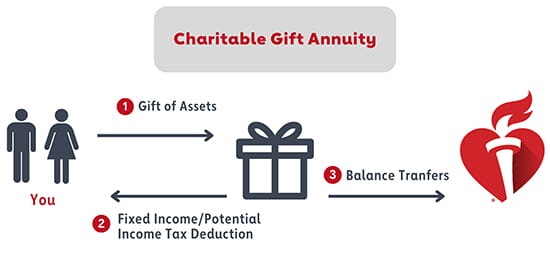

Many charitable organizations offer charitable gift annuities to their benefactors to provide income during the life of the annuitant, with the remainder going to the organization. It is generally a sweet deal for both – a tax deduction and guaranteed income for the donor, with the remainder interest of the annuity for the charity.

Key components and benefits to a Charitable Gift Annuity.

Let’s step back and understand the structure of a charitable gift annuity (often referred to as a CGA).

- In exchange for an asset, the donor or annuitant is guaranteed a fixed income stream for one or two lives for the remainder of their lifetime(s), or for a term of years.

- The rate of the charitable gift annuity is based on the annuitant’s age, or a blended rate for a two-life annuity. Most organizations use the suggested maximum rates published by the American Council on Gift Annuities (ACGA). These rates are designed to produce a target gift for charity at the death of the annuitant(s) equal to 50% of the amount of the annuity.

- The income is often partially taxable and non-taxable. This is generally determined by the age of the annuitant and the assets that fund the charitable gift annuity.

- Funding assets include cash, stocks, bonds, mutual funds, real estate, and a variety of other assets.

- Income can begin immediately, or it can be deferred to a point in the future based on the financial considerations of the donor. This option is most often used by younger donors, who frequently chose to begin their payments after retirement as a means of supplemental income.

- The minimum age for immediate payment annuities is generally 65, but it varies depending on the charity.

- Gift minimums are also determined by the charity but may be as low as $5,000.

- The payments are generally backed by the full assets of the charity.

Download your Charitable Gift Annuity overview (PDF).

Charitable Gift Annuity or Charitable Remainder Trust—which solution is right for your client?

A charitable remainder trust (CRT) is another charitable solution to consider. While the benefits are comparable to a CGA, there are additional costs associated with a charitable remainder trust, including the cost to establish the trust and yearly fees for investment management and tax reporting. In contrast to a CGA, the charitable trust payout rate can be flexible and the remaindermen of the trust can go to more than one charity. The donor can also retain the right to change the remaindermen from one charity to another.

With an understanding of both charitable solutions, which do you suggest to your client? The answer lies with your donor and the dollar amount of the gift. The advantage of the CGA is its simplicity. Generally, the charitable gift annuity is established with no cost to the donor, limited paperwork, no future fees, and no tax preparation fees. The donor will receive a 1099 from the charity for tax purposes. Many advisors recommend a charitable gift annuity for a smaller gift—$250,000 or less—but this life income gift works well for larger amounts as well. If your client likes things simple and easy, the charitable gift annuity is the answer.

Using a Charitable Gift Annuity in a financial plan.

How would you use a charitable gift annuity in a financial plan as compared to a tax-free bond, a U.S. treasury bill, bond, note, or a corporate bond? There are a few aspects to consider. First, it’s important to remember that a CGA is not an investment, it is a life income charitable gift. For a CGA to be a good fit in your client’s financial plan, your client should have charitable intent; the remainder of the annuity will be payable to the charity that issued it. Second, your client should be seeking a fixed income for a certain number of years or for their lifetime. Finally, your client should have additional assets to support their lifestyle or medical expenses.

Let’s look at an example. Your client, Sue, age 82, wishes to increase her income and is a devoted, longtime supporter of the American Heart Association. Based on Sue’s age, her payout rate would be 8.1% and with an income tax bracket of 22%, this is like receiving a 10.96% taxable return. If Sue funds the annuity with $100,000, she will receive a tax deduction of $52,747. Sue would also receive $8,100 per year, with $5,621.40 of this annual amount qualifying as tax-free until the end of year 2030. After that, the entire payment would be taxable.

What the Legacy IRA Act could mean for your clients.

The Legacy IRA Act, as part of the SECURE Act 2.0, which became effective January 1, 2023, creates new charitable gift planning opportunities for donors starting at age 70.5. The act expanded the definition of qualified charitable distributions to include certain distributions to create life income gifts, specifically charitable gift annuities and charitable remainder trusts.

The bill allows IRA owners to make a one-time distribution for a charitable gift annuity or charitable remainder trust. This is limited to a maximum of $50,000, and although not limited to a single gift, must be completed in a single year and only once during the lifetime of the IRA owner. Due to the limitation of the amount, a charitable gift annuity would be the low cost and simplest solution.

Download your Legacy IRA Act overview (PDF).

A charitable gift annuity is a way for your clients to benefit financially while helping others. This charitable gift option provides future funding for the mission of the charity that is near and dear to the heart of your client. In exchange, your client receives favorable income tax benefits and a guaranteed income stream for life.

Our team of advisors at the American Heart Association can provide you with free illustrations and information on the benefits of a Charitable Gift Annuity as well as the Legacy IRA Act. Find an advisor in your area or call 888-227-5242 and we will be happy to help.

About the Author

John W. Cullum, CFP®

John W. Cullum, CFP®

Senior Charitable Estate Planning Advisor

[email protected]

864-517-2154

John is based in Charlotte, North Carolina, and serves the southern states.

After a 35-year private banking and trust career, John, a Certified Financial Planner ®, took early retirement and decided to do something that would make a difference. He worked in college fundraising and has dedicated the last seven years to the American Heart Association, where he collaborates with professional advisors to connect the philanthropy of their clients with the mission of the association. He has served on numerous philanthropic boards, most recently the Charlotte Garden Club.

John is a graduate of the University of South Carolina and University of North Carolina at Chapel Hill Young Executive Institute. John has two adult sons, a 6-year-old granddaughter, 3-year-old Plott Hound and is an avid gardener.